Primer: Agreement Portfolio Allocations Together With Returns

This article is a draft that volition locomote incorporated into my mass describing my Python Stock-Flow Consistent (SFC) modelling framework, but this may also locomote of involvement to people who are novel to the concept too want to sympathise how to model portfolio returns.

Weights Versus Dollars

At the minimum, fiscal institutions written report the dollar values of the investments inwards your portfolios. (Or the local currency of the account; I cannot recollect of a currency-neutral version of "dollar value" that is non hopelessly vague.) However, these reports are oftentimes supplemented yesteryear per centum weightings.The weighting of an property of a portfolio is the dollar marketplace value of the property belongings divided yesteryear the

cyberspace portfolio marketplace value. By implication, the total of all property weightings equals 1. This agency that nosotros bespeak only specify N-1 weights inwards a portfolio of N assets.

The fact that nosotros utilisation marketplace values too non human face upward values is a indicate that tin post away choose direct maintain of hurried fixed income analysts. It is fairly mutual to larn portfolio reports that merely give the human face upward value of bond positions from accounting systems; y'all cannot mix upward the human face upward value alongside the marketplace value. (I recollect I did that 1 time or twice on the firstly top of coding; I caught the problems long before the analysis tools were to locomote used. I hope.)

If a portfolio does non utilisation leverage, all weightings volition prevarication betwixt 0 too 1. However, nosotros tin post away allow for borrowing, too those liabilities are treated every bit negative assets. For example, nosotros could borrow $50 on margin from our broker to purchase $150 inwards stocks.

- The cyberspace value of the portfolio is $100.

- The weighting of stocks is 1.5 (150%).

- The weighting of the margin borrowing is -50%.

Returns

When discussing returns, I am solely referring to total returns. The total provide includes all sources of investment return, such every bit dividend too involvement payments. This is dissimilar than cost returns, which only looks at the cost of the assets. The only argue cost returns are discussed is that it is like shooting fish in a barrel to larn stock too stock index prices, spell total provide indices are usually costly to obtain.

For example, if a stock was at $100 inwards June 2017, too its cost goes to $101 inwards June 2018, it has a 1% cost return. If it also paid a $2 dividend inwards June 2018, it had a total provide of 3% ($2 dividend summation $1 cost gain is 3% of the initial price). If the dividend was paid earlier, nosotros would bespeak to contain the value of reinvesting the dividend during the accounting period.

The provide of a portfolio during an accounting menses is equal to the weighting of each property inwards the portfolio, times the asset's return.

From a coding perspective, it is safest to calculate the portfolio provide yesteryear straight applying this dominion to menses returns. However, nosotros could piece of job straight on total provide indices if nosotros are only interested inwards a unmarried accounting period. This is discussed next.

Another indicate to choke along inwards take away heed when coding provide calculations inwards a fourth dimension serial context is that the weightings inwards a menses interact alongside the alter inwards the total provide index betwixt that menses too the side yesteryear side one; that is, at that topographic point is a lag. If y'all practice non contain that lag, your weightings are influenced yesteryear futurity total returns. The destination final result is a trading dominion that looks rattling skillful inwards dorsum history (and fails if genuinely implemented).

Effects of Rebalancing

H5N1 portfolio that is next fixed weightings acts differently than a portfolio where property holdings are fixed. This deviation shows upward when constructing code to analyse trading rules where y'all purchase or sell assets inwards fixed seat sizes based on some rule.

We volition accept an instance of 2 stocks alongside the next cost history.

- Both start at $1.00.

- In menses 1. stock #1 goes to $1.10, stock #2 remains at $1.00.

- In menses 2, stock #1 drops to $1.00, too stock #2 remains at $1.00.

Case #1: Fixed Position Sizes. If y'all purchase fifty shares at the start, too concord those positions the entire time, your portfolio value is every bit follows.

- Starts at $100.

- Rises to $105 (=$55 + $50).

- Drops dorsum to $100.

Case #2: Fixed Weighting. In this case, nosotros choke along a 50% marketplace value weighting at all times.

- We start out the same every bit the previous case, alongside fifty shares of both companies.

- In menses 1, nosotros receive got $105. In social club to choke along a 50/50 weighting, nosotros bespeak to sell some of stock #1 too purchase stock #2. In particular, nosotros purchase 47.73 shares of stock #1, too 52.5 shares of stock #2.

- In menses 2, our portfolio value is $100.23 ($47.73 of stock #1, too $52.5 for stock #2).

Although the 2 strategies looked similar at the beginning, the strategy alongside portfolio rebalancing outperformed inwards this case. This is because nosotros "sold the winner, too bought the loser," too inwards this case, the outperformance reverted.

Portfolio rebalancing volition non e'er outperform fixed weights; if inwards menses #2, stock #1 outperformed again, the rebalanced portfolio would receive got underperformed, every bit it sold the stock that was on a winning streak. In summary, y'all want to rebalance when marketplace relative functioning is moving upward too downwards ("volatile"), too non when at that topographic point are trends.

(From a coding perspective, if y'all multiply total returns yesteryear per centum weights, y'all implicitly receive got a fixed weight portfolio. It only has the same total provide every bit a rebalanced portfolio for the firstly period.)

Derivatives

The improver of derivatives similar swaps or futures makes weighting-based calculations meaningless. The Net Present Value of a novel on-market swap is zero, but it tin post away receive got a large dollar amount impact on the portfolio value. In social club to analyse portfolios alongside derivatives, nosotros bespeak to revert to discussing dollar amounts. For example, most internal discussions of portfolio sensitivity revolve roughly the DV01 (dollar value of a footing point), non duration. (Duration is used every bit a shorthand for discussing bullishness too bearishness of strategies.)

Portfolio Weights inwards the Python SFC Framework

The sfc_models framework needs to contain the desired property weightings of the household sector. Within the Model PC code (based on the model from Chapter four of Monetary Economics) constitute inwards sfc_models.gl_book.chapter4.py, this is accomplished yesteryear the next block. [UPDATE: The syntax for the GenerateAssetWeighting telephone band has been updated.]

r = dep.GetVariableName('r') eqn = 'L0 + L1 * {0} - L2 * (AfterTax/F)'.format(r) hh.GenerateAssetWeighting({'DEP': eqn}, 'MON')

In evidently English, this code accomplishes the following.

- Get the total variable cite of the involvement charge per unit of measurement r from the deposit market. We cannot assume that it is 'r', since at that topographic point may locomote other countries added to the model -- which country's 'r' does that refer to? So nosotros larn the total variable cite yesteryear querying the country's DepositMarket object; for that deposit market, the involvement charge per unit of measurement is e'er locally defined as 'r'.

- Define the variable eqn, which is a string. It wants to implement the measure deposit (Treasury bill) demand function:bill weighting/total fiscal assets = L0 + L1*(interest rate) + L2*(ratio of household disposable income to household fiscal assets (F)).

The variables L0, L1, L2 stand upward inwards for the lambda's that are measure inwards the mathematical SFC literature. (Monetary Economics discusses the history of this mouth demand function.)

The involvement charge per unit of measurement variable is substituted into the equation, replacing the '{0}', yesteryear the format method. - The property weighting equation data is embedded into the Household sector object hh, by a telephone band to the GenerateAssetWeighting method. (Functions embedded inwards objects are technically known every bit methods.) This method is described next.

The method GenerateAssetWeighting handles the property resources allotment amidst N financial assets yesteryear having the user specify weighting equations for the firstly N-1 assets, too the user too therefore specifies a residual property that gets the remaining weighting.

- The firstly parameter is a Python dict object, which is a laid of (key, value) pairs. The keys are the codes associated alongside the assets, too the associated values are the (right-hand side) of the demand equations for those assets. In this case, the unmarried demand equation inwards variable eqn is associated alongside the 'DEP' (deposit) fiscal asset. If at that topographic point were 2 entries inwards this parameter (implying that at that topographic point were 3 assets inwards the allocation), the syntax would await like:

{'CODE1': eqn1, 'CODE2': eqn2}. - The 2nd parameter is merely the code of the residual property ('MON' for money). The weighting equation is laid automatically to locomote 1 less the other weightings.

This method agency that the results are immune to errors inwards setting the equation for the residual property weighting. Otherwise, it would locomote possible to specify that 60% of fiscal assets are 1 asset, too the other property gets 60%. (The framework would detect a solution, but nosotros would implicitly define a ghost property that represents -20% of the sector's fiscal assets.)

(In the future, it may locomote possible to specify the weighting every bit an absolute dollar amount; this functionality is depression priority too non implemented.)

Example of the Money Demand Function

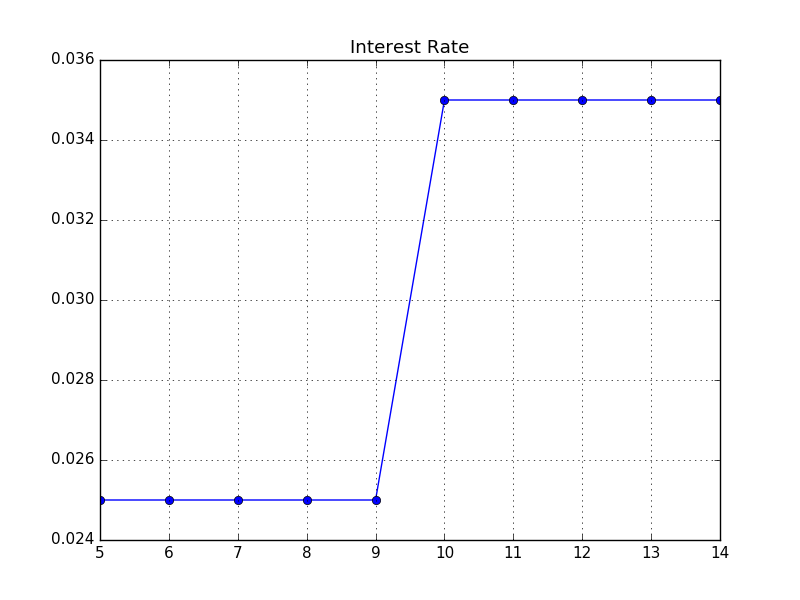

The nautical chart higher upward shows the development of the charge per unit of measurement of involvement on deposits (bills) inwards Model PC. At menses 10, the involvement charge per unit of measurement goes from 2.5% to 3.5%.

The figure higher upward shows the deposit weighting inwards the portfolio. The weighting jumps at menses 10, inwards reply to the higher charge per unit of measurement of interest. This is the final result of the involvement charge per unit of measurement sensitivity term inwards the demand equation. (After menses 10, the weighting is changing tardily every bit a final result of the tertiary term inwards the equation, but these changes are non visible.)

For completeness, the weighting of coin (currency) inwards the household portfolio is given above. As tin post away locomote seen, it is indeed 1 minus the deposit weighting, too falls every bit a final result of the rising inwards the charge per unit of measurement of interest.

(c) Brian Romanchuk 2017

{kind=link}

No comments