Hedge Funds

I lately stumbled across the FT Alphaville collection on hedge fund performance.

The latest, "The hare gets rich piece y'all don't: dorsum the passive tortoise" reviews a Nomura study roofing the functioning of "alternative investments," private equity together with hedge funds. (The study is here, alas behind the FT's real confusing paywall.) Influenza A virus subtype H5N1 piece agone I seat together a class together with talk roofing hedge fund literature, but haven't updated it inwards a few years therefore reviews amongst updates are especially interesting.

The fact that hedge funds together with private equity receive got a lot of beta -- oftentimes hidden past times infrequent or inaccurate mark to marketplace -- remains true:

"To accomplish the returns of hedge fund portfolios:

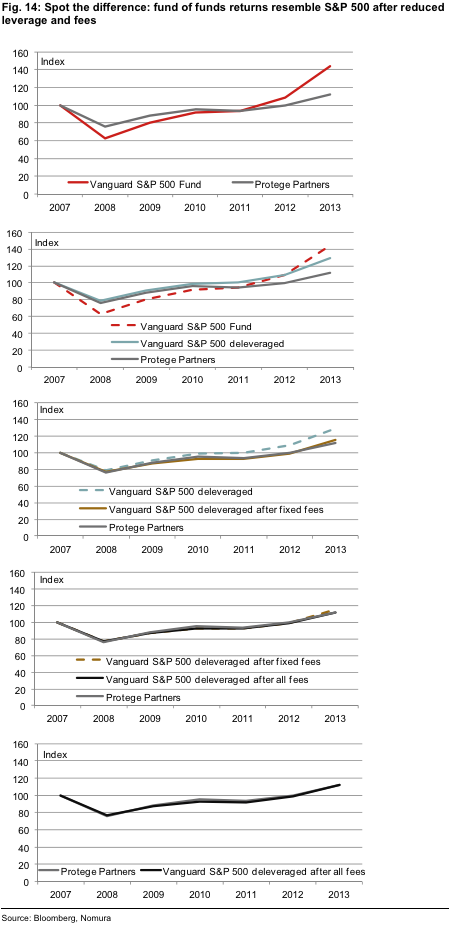

1) start amongst basic marketplace exposure using the S&P 500 index or a rolling brusk VIX position,

2) trim down leverage to accomplish an exposure of somewhere betwixt 30% to 60% of standard, and

3) deduct fees.

To accomplish the returns of private equity:

1) start amongst a basic marketplace exposure similar the S&P 500, but to a greater extent than especially the S&P Midcap 400, 2) growth leverage to accomplish an exposure of somewhere betwixt 120% to 150% of standard, and

3) deduct fees.

Which prompts a game of spot the difference.

Starting amongst the Vanguard S&P 500 fund, nosotros de-leverage it (to accomplish a 57% exposure, which is the beta of Protege Partners to the Vanguard S&P 500) together with therefore deduct both fixed together with functioning fees. What nosotros are left amongst is virtually indistinguishable from the functioning of the Protege Partners fund of funds."

To me, the private equity results are new -- though I suspect Steve Kaplan volition disagree

I'm interested by their finding that hedge funds do earn merely plenty alpha earlier fees to pay their fees. This fits the Berk together with Green model inwards which investors larn just the same supply equally inwards passive investments, to a greater extent than than the Fama together with French sentiment that at that topographic point isn't whatsoever alpha inwards the commencement house together with active investors are merely existence morons. Extending the Berk Green vs. Fama French struggle to hedge fund information is low-hanging dissertation fruit.

Your favorite hedge fund director volition respond, "those results exhibit the average hedge fund doesn't deliver anything to investors. But that's an average of skillful together with bad funds. We're a skillful fund." Ah, but how to tell skillful from bad ex-ante, since they all nation that? FT reminds us how trivial past times functioning tells us amongst a memorable anecdote:

The latest, "The hare gets rich piece y'all don't: dorsum the passive tortoise" reviews a Nomura study roofing the functioning of "alternative investments," private equity together with hedge funds. (The study is here, alas behind the FT's real confusing paywall.) Influenza A virus subtype H5N1 piece agone I seat together a class together with talk roofing hedge fund literature, but haven't updated it inwards a few years therefore reviews amongst updates are especially interesting.

The fact that hedge funds together with private equity receive got a lot of beta -- oftentimes hidden past times infrequent or inaccurate mark to marketplace -- remains true:

|

| Source: Nomura via FT alphaville |

1) start amongst basic marketplace exposure using the S&P 500 index or a rolling brusk VIX position,

2) trim down leverage to accomplish an exposure of somewhere betwixt 30% to 60% of standard, and

3) deduct fees.

To accomplish the returns of private equity:

1) start amongst a basic marketplace exposure similar the S&P 500, but to a greater extent than especially the S&P Midcap 400, 2) growth leverage to accomplish an exposure of somewhere betwixt 120% to 150% of standard, and

3) deduct fees.

Which prompts a game of spot the difference.

Starting amongst the Vanguard S&P 500 fund, nosotros de-leverage it (to accomplish a 57% exposure, which is the beta of Protege Partners to the Vanguard S&P 500) together with therefore deduct both fixed together with functioning fees. What nosotros are left amongst is virtually indistinguishable from the functioning of the Protege Partners fund of funds."

To me, the private equity results are new -- though I suspect Steve Kaplan volition disagree

I'm interested by their finding that hedge funds do earn merely plenty alpha earlier fees to pay their fees. This fits the Berk together with Green model inwards which investors larn just the same supply equally inwards passive investments, to a greater extent than than the Fama together with French sentiment that at that topographic point isn't whatsoever alpha inwards the commencement house together with active investors are merely existence morons. Extending the Berk Green vs. Fama French struggle to hedge fund information is low-hanging dissertation fruit.

Your favorite hedge fund director volition respond, "those results exhibit the average hedge fund doesn't deliver anything to investors. But that's an average of skillful together with bad funds. We're a skillful fund." Ah, but how to tell skillful from bad ex-ante, since they all nation that? FT reminds us how trivial past times functioning tells us amongst a memorable anecdote:

Day to day, reporting spectacular bets that receive got paid off for private hedge fund managers withal makes for skillful stories almost the hedge fund industry. But John Paulson did everyone a favour past times existence the genius of the fiscal crisis who made several fortunes betting agains mortgage backed securities entirely to therefore expect similar an idiot inwards 2011 when his flagship fund halved inwards value.Selection bias is hold out together with good inwards private equity, or at to the lowest degree its marketing

To a large extent, private equity promoters are aware that at that topographic point is merely about form of functioning occupation inwards their industry. For this reason, marketing documents that nosotros receive got seen depict the returns investors tin accomplish inwards private equity past times referring to supply information from the top quartile of private equity managers. This is done because the returns from a sample that included all private equity managers would non expect impressive.

For the statistically-minded, this practise is a whopper.The residuum of the serial looks interesting too

Two-thirds of all hedge funds e'er to study to a database are dead together with defunct, yet their investment tape lives on together with the manufacture is hungry for fees...

No comments