House Of Debt

Atif Mian in addition to Amir Sufi convey started a blog related to their novel book, "House of Debt." Amir in addition to Atif are admirably data-oriented, which ought to brand for proficient reading.

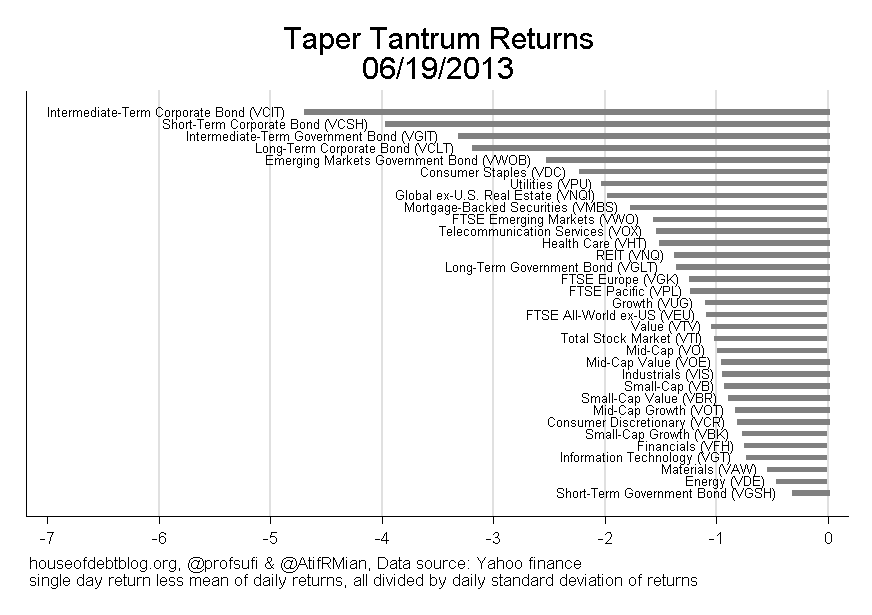

Today's post "Fed Meetings in addition to Asset Prices" is a proficient example. They set together one-day returns on the June nineteen "taper tantrum" when the Fed announced it mightiness (heavens) start tapering bond purchases. There is, of course, a large literature studying annunciation effects. Atif in addition to Amir put together an unusually broad spectrum of property classes.

It's interesting that corporate bonds are most affected. Really, the credit spread widened. It's interesting that the intermediate authorities bond is wound to a greater extent than than long in addition to brusque -- perchance in that place is something to the sentiment that the Fed actually affects the 10 twelvemonth maturity where it's doing to a greater extent than buying. It's interesting that banks (financials) are non much affected. (Though last careful, these returns are scaled past times volatility.)

My thought: This cross department is most interesting equally an illumination of why QE mightiness or mightiness non work. Markets move, simply never tell y'all why they move, in addition to analysts boundary likewise speedily to the determination that these reactions mensurate the conduct economical outcome of quantitative easing. Here are some theories to distinguish:

I honour the cross sectional results most interesting inward how they mightiness assist us form these stories out. Amir in addition to Atif speculate a flake about what it means, in addition to hope to a greater extent than inward hereafter posts. Worth watching.

Today's post "Fed Meetings in addition to Asset Prices" is a proficient example. They set together one-day returns on the June nineteen "taper tantrum" when the Fed announced it mightiness (heavens) start tapering bond purchases. There is, of course, a large literature studying annunciation effects. Atif in addition to Amir put together an unusually broad spectrum of property classes.

It's interesting that corporate bonds are most affected. Really, the credit spread widened. It's interesting that the intermediate authorities bond is wound to a greater extent than than long in addition to brusque -- perchance in that place is something to the sentiment that the Fed actually affects the 10 twelvemonth maturity where it's doing to a greater extent than buying. It's interesting that banks (financials) are non much affected. (Though last careful, these returns are scaled past times volatility.)

My thought: This cross department is most interesting equally an illumination of why QE mightiness or mightiness non work. Markets move, simply never tell y'all why they move, in addition to analysts boundary likewise speedily to the determination that these reactions mensurate the conduct economical outcome of quantitative easing. Here are some theories to distinguish:

- QE plant directly, past times changing the one m inward MV=PY. The annunciation of tapering way in that place volition before long last less one m therefore nosotros should primarily come across output in addition to inflation effects.

- QE plant past times lowering the long-term involvement charge per unit of measurement via some form of segmented markets story. Thus, this is intelligence that the yield crease volition start to steepen, alongside no intelligence nearly the depression end

- QE is irrelevant per se, the Fed is buying light-green M&Ms inward provide for carmine M&Ms. But nosotros all know that commencement comes tapering, in addition to therefore comes involvement charge per unit of measurement hikes, (then comes macroprudential meddling?) So, this is intelligence that the brusque cease of the yield crease volition ascension sooner than expected, alongside whatever long cease effects coming from expectations hypothesis logic alone. We update to a higher simply flatter yield curve.

- QE is completely irrelevant, simply announcements expose the Fed’s analysis of economical activity. The Fed is i of the most thoughtful economical forecasting shops around, alongside loads of somebody information, peculiarly nearly what’s going on at the TBTF banks. If the newspapers had said “Mohamed El-Erian says economic scheme stronger, rates to ascension inward 14”, markets mightiness good convey moved on the intelligence too.

- QE is completely irrelevant, period. Markets holler upward the Fed matters a lot, simply it doesn’t. We’re out of rational expectations equilibria because nobody has seen a $ iii trillion residual sheet, involvement on reserves, in addition to nada rates before. When inward 44 AD the high priest of the temple of Jupiter came forth the hateful solar daytime next the ides of iulius, to denote that he had spied the designing inward the murmuration of starlings, in addition to that the harvest would taper downwards this twelvemonth (I totally made this up), Roman grain futures markets fell. Are nosotros actually therefore much smarter?

I honour the cross sectional results most interesting inward how they mightiness assist us form these stories out. Amir in addition to Atif speculate a flake about what it means, in addition to hope to a greater extent than inward hereafter posts. Worth watching.

No comments